Everything you need within a single platform

Safety and security

Make sure your drivers, vehicles, and assets are safe.

Compliance

Follow all rules, including tachograph regulations, with ease.

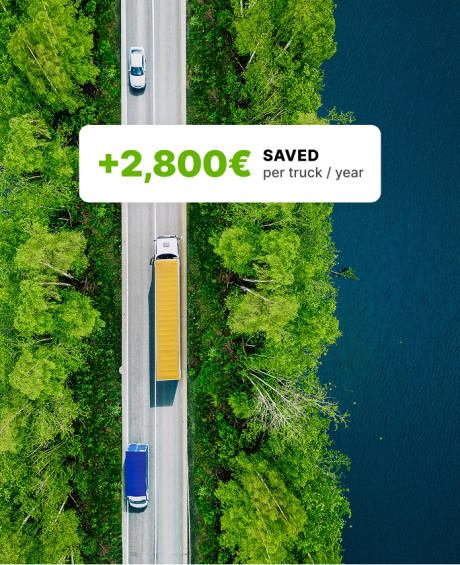

Cost optimisation

Decrease costs by optimising fuel consumption and fleet maintenance.

Process automation

Make your processes faster and remotely accessible.